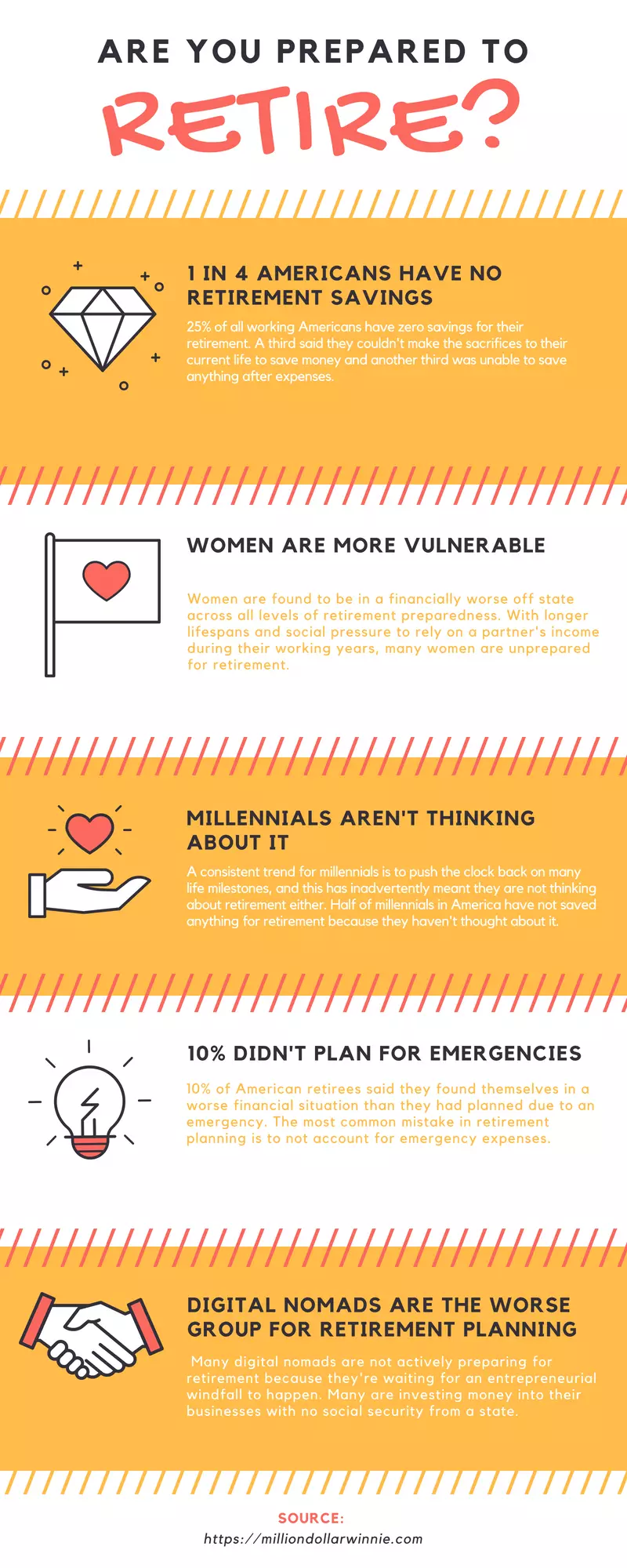

What is up hustlers. It’s nearing June which means we’re at the half way point of 2018, and sometime in the 4th quarter of 2017 I announced my Goliath goal of retiring by the age of 35.

I just put it out there with no plan or idea on how I’ll do it. I only knew what I wanted and defined the parameters of what I wanted by giving a clear vision of what retirement looked like for me.

So today, I’m actually going to create a plan. A plan I will follow and a plan YOU can use as a template to plan your own retirement.

(you’re welcome)

You may want to save this to Pinterest because this is going to be a lot to take in if you’re reading it in one go.

Figuring out your timeline

First things first, you need to figure out the time. Retirement planning only works if you know how old you want to be when you retire. That will define how much time you have to prepare for retirement.

For me that’s 9 years and a bit to make this happen. (Yes, I know it’s a lofty goal…but people need to have dreams in life to make it interesting)

Next you need to estimate your life span. When you have this number you’ll know exactly what you need to financially prepare for.

Someone retiring at 60 and estimates their lifespan at 80 only needs to prepare for 20 years of financial security. That person will do completely different things to a person who wants to retire at 40 and estimates their lifespan at 80.

For me, my natural lifespan would most likely reach 90. That means I will need to prepare for 55 years of financial security. Now before you think those are ridiculous numbers, you can read my post where I defined my visions of what retirement means to me. (Hint, it’s not me doing absolutely nothing on a beach everyday)

You can estimate yours by noting the age when your family members have passed away. Grandparents, parents, aunts and uncles. And then of course take into account any hereditary chronic illnesses and your current living habits.

Deciding what type of retirement you want

I already did this part in my other post, but a quick recap so you can follow along with me.

Since I want to retire by 35, I’ll still most likely have many financial responsibilities to deal with. Such as ageing parents and young kids. I would most likely be physically, mentally and emotionally fit, which would make doing nothing extremely hard and wasteful.

That’s why my idea of retirement by the age of 35 is to work, not because I have to, but because I want to. I want to be able to spend most of my time with family and friends without needing to worry about my livelihood.

I’d like to have the time freedom to explore what life has to offer in terms of hobbies, opinions, cultures and various walks of life. I’d like to have the resources to help others and do projects that give back in a very direct manner.

That means travelling to new places, trying new things and learning new skills.

In summary, I want to achieve my goal of 360 balance. If you’re new to the site and haven’t read my about me page, then you might not know what 360 balance means.

It means:

The physical health to have the freedom to do what I want.

The financial freedom to do what I want whenever I want.

The mental freedom to never be afraid to go after what I want.

And lastly the social freedom to make my own decisions on what I want.

There’s going to be limitations to the above from ageing and life naturally, but for the most part that is how I define retirement. It’s the closest thing to freedom you can achieve without being destructive to yourself or to others.

Another thing to note in my case, is that I will most likely not keep this definition of retirement for the whole duration of my retirement. I most likely won’t have the physical, mental and emotional health to keep working by the time I’m 70 or 80.

I will only want to spend my days in a relaxed manner, enjoying what I have achieved and not in the mindset of still trying to push myself to reach new heights.

So that’s 35 years of wanderlust retirement and 20 years of text book definition retirement.

Picture your own retirement life as detailedly as possible before you proceed, because the usefulness of your numbers will rely on how clear of a goal you have.

The two types of money you need for retirement

I’m living in Hong Kong as I write this and I’m self-employed. Which means this guide is not going to include 401K, IRAs or any other American retirement social security plan. Hong Kong has this thing called the MPF, it’s pretty crap and I’m not even going to include that into my calculations.

Most countries will have some form of a retirement fund that is overseen by the government. Some countries will also have some form of a pension or monthly financial aid to those that reach retirement age.

I won’t be taking these into account. Why?

One, Hong Kong’s pension is an insignificant amount and you would have to be in a poor financial state to even qualify to get it. (I have no intention to have a breadline retirement)

Two, you guys come from all over the world and this guide wouldn’t be practical if it wasn’t applicable to most.

However, if you do live in a country where social security isn’t half bad, then you should educate yourself on the matter and take it into account.

Third, a lot of people actually don’t retire in the same place they work. Overseas retirement is becoming more and more common and state pensions or funds wouldn’t really apply for most cases. Again it depends on the local laws of your country on whether pensions can be given to oversea citizens.

Moving on.

Since I will approach this with no intention of relying on a pension or a fund for financial security. I will be relying on 2 things.

- Savings

- Passive income streams

Savings

No one got rich from saving alone, and you definitely won’t be able to retire from savings alone either. It’s also not very secure.

If savings are the only asset you have, then your cashflow is going one way, out. Your balance will only be going down, and that’s not good because it leaves you vulnerable to the unexpected.

Unexpected emergencies. Unexpected lifespans. Unexpected economic events.

However, savings in the form of an emergency fund or as a monetary airbag for the unexpected is great. What I mean is, you’ll still want a certain amount of liquid cash, ready for immediate use for the unexpected.

YOU DON’T want to have liquid cash to be funding your predictable and planned retired life.

Passive income

That’s where passive income comes in. You want passive income to be funding your planned and predictable part of retirement.

Passive income is derived from some form of an asset. Not all assets will derive passive income so let’s go over some common examples of assets that do provide passive income.

Real estate: Real estate can provide you passive income in the form of rental income.

Stocks: Most stocks provide annual, or quarterly dividends that provide passive income to live off from.

The above two are the most common forms of passive income retirees tend to use. There are many others and thanks to technology I’m able to enjoy passive income at such a young age, but how you go about creating passive income in your life will be your own individual choice. There’s just too many ways to talk about it in this post. You can check out my comprehensive list of 100 passive income methods here to get some ideas.

Because passive income is reliant on an asset, where an asset is anything of value that can be sold for cash; passive income isn’t great for unexpected events and expenses because it takes time to turn assets into cash. And you shouldn’t have such a large amount of passive income that you can handle your usual expenses as well as the unexpected.

I say you shouldn’t because it takes time, effort and upfront money to create passive income. In terms of retirement, there is such thing as having too much. Having too much passive income will inadvertently mean you’re not using your resources as efficiently as possible and it also means you’re making yourself work harder to achieve retirement.

Calculating how much you need in savings

Now it’s time to figure out how much money you need to make the above happen. This is the hard part. Everything above was to set the parameters of your calculations, now it’s time to actually start calculating.

Let’s start with savings.

As pointed out from the above, savings are for emergencies that happen in life. You don’t know when they’ll happen, but they will definitely happen in your life.

Because you can’t plan for them, there is always a margin of error in your calculations here. You will have to accept this. Some people think by taking the most pessimistic view on life, they can plan appropriately, but that’s false.

Just like having too much passive income, you can have too much savings. It means you’re not using your money efficiently and makes retirement a harder goal to achieve.

The type of emergencies I will be saving for are ones I think are realistically going to happen at one point or another. These include medical bills, repairs and replacements around the house, legal fees and other one off professional service fees, helping family members financially for unexpected events.

The above should apply to most people’s situations as well.

When you calculate the above, you will want to think about your external environment to provide an educational guess on how many times it may occur in your life as well as at roughly what time in your life it will occur.

The second part of that sentence isn’t as obvious for most people, but at what time an emergency happens will influence your financial status quite a bit. For example, large medical bills at a relatively young age will put you in greater danger of financial insecurity than if you have those medical bills at an older age.

Why? because if you had $10 in emergency funds and you were already 80 years old with medical fees of $5. You will only need the other $5 to last you, another decade or so. But at age 50, you need the same $5 to last you 40 years, if you are assuming your lifespan is 90 like me.

Of course, your emergency fund shouldn’t be created and then left alone. You should be reviewing it and adjusting the amount accordingly throughout your retirement, but we’ll talk about that a little later down the post.

While you calculate these numbers you will also need to think about inflation so your emergency fund won’t be completely useless.

For a simple way to calculate how much you need in savings for an emergency fund. Simply save 2 years worth of expenses. 2 years worth of expenses will change throughout your life, which is why I said your emergency fund needs to be regularly reviewed and then tweaked.

For me I’ll be making estimates for different age brackets of 35 – 58, 59 – 70, 71 – 80, 81 – 90. I’ve created the age brackets according to realistic estimations of my life situation, health and likely events to happen.

My estimates:

For the ages of 35 – 58: 2,000,000 HKD in today’s purchasing power (254,790 USD)

I put purchasing power because I want to make clear that you want to maintain your purchasing power, which means you will need to have more cash over time since inflation will decrease the value of money over time.

$10 bought you more things a decade ago than compared to $10 in todays money.

That means while I’m saving the above amount, I will have to account for inflation to maintain my purchasing power. It would mean the basic rudimentary calculation of $2,000,000/9 years will give me a lot less than what I wanted.

To reach $2,000,000 HKD in todays purchasing power in 9 years at the age of 35 with an annual inflation rate of 3%, I will need $2,533,540 HKD.

And then I will be adjusting the amount according to my life situation as time goes on.

The above numbers might look huge for some, but I’ve calculated the numbers based on the cost of living in Hong Kong. (which isn’t the cheapest if you want a comfortable middle class level of living)

Calculating how much you need in passive income

There’s a reason why you should calculate your emergency fund first. It’s because it makes this part a lot easier.

Take $2,533,540 and divide it by 24. That will give me the estimated amount of my monthly expenses at the age of 35. That’s around $105,600 HKD.

Now an emergency fund is suppose to be modest in nature because it’s for emergency only and shouldn’t take into account too many luxuries. Therefore, I’ll 4 times the amount to achieve the lifestyle I want. Normally that would be unwise and ridiculous, but I’ll be 35. I am nowhere near downsizing and the fact is my expenses will be increasing with young children and ageing parents to take care of.

That gives me the amount of $422,400 HKD (54,000 USD). Admittedly, $422,400 HKD per month will provide a very luxurious lifestyle for me, my parent and my yet to exist family. But it’s good to aim higher on this part.

Shoot for the moon and if you miss you’ll still be among the stars.

What type of passive income do you want?

$422,400 HKD is the amount my assets will need to be providing me on a monthly basis. Now you need to figure what type of assets you want to achieve this number.

I’ll like 5 kinds of passive income to be in my portfolio. They are:

- Dividends

- Rent

- Royalties

- Sales

- Commissions

But realistically, I probably won’t be able to have all 5 by the age of 35. So by the age of 35, I’ll like the following kinds of passive income in my portfolio:

- Dividends – From stocks on the market and stakes held in small businesses as a limited partner

- Royalties – From my publications on KDP, ACX and Createspace

- Sales – From POD and drop shipping businesses based online

- Commissions – From affiliate marketing websites I run

The above leaves me a little vulnerable because most of the above passive income I am choosing to pursue are online based. They are new with very little understanding from greater society and so if I ever wanted to liquidate these assets, there will be more of a challenge. The value of the asset itself will also be lower than an offline asset that derives an equal amount of passive income.

That’s why, eventually I want to add in real estate rental income to my portfolio as well, so I know if there was any extreme change of event in my life, I can just liquidate my assets to have money to live off on. However, I won’t include too many details of that here because it’s unlikely I will have investment real estate by the age of 35. It’ll have to be something I continue to develop after I retire.

The breakdown

- Dividends – Accounting for 5% of total passive income (2,700 USD)

- Royalties – Accounting for 10% of total passive income ( 5,400 USD)

- Sales – Accounting for 55% of total passive income (29,700 USD)

- Commissions – Accounting for 30% of total passive income (16,200 USD)

The above is the desired percentage breakdown on how much each type of passive income will equate to to the total amount.

Those percentages weren’t randomly selected, and when you figure yours out you shouldn’t be mindlessly putting numbers down. These numbers are targets for you to focus on and so they should be:

- Practical and realistic to achieve

- Places you in the most secure financial position

Like I had mentioned above, 3 out of the 4 are based online and require low capital investments to build. (In comparison to more traditional asset acquisition methods.) Being a young person with a short period of time to achieve my goal, the last 3 types of passive income are going to be my focus point.

Achieving anymore than 5% of my total passive income in dividends would require a lot of effort to raise the upfront capital needed to acquire it on top of the cash I need to save. It’s just simply not realistic for my situation.

You’ll want to evaluate your own situation to understand how your portfolio should look like to be the most effective.

Dividends

Because dividends tend to come from assets that require large upfront capital, we’re going to have to examine this part in more detail.

Dividends from stocks on the market or shares in a small business are the most common ways to receive dividends in your life. Dividends from small business investments will be something of a serendipity opportunity.

It depends on who you know and what your social circle is like, so we’ll ignore that kind. Instead, we’ll just focus on the dividends you get from stocks on the market.

Some companies will give out dividends to their shareholders and the amount they give is called the dividend yield. This is in percentage and can range from 0% all the way to 10%+. A reasonable low risk high yield stock portfolio should achieve around 5% – 6% and after taxes, fees and the like, you should have at least 3% in your pocket.

The above are very typical numbers that are achieved by most people.

If you were to use the above to make assumptions about how your portfolio will behave than $254,200 HKD ($2,700 x 12 = 32,400 USD) should be equal to a 3% net yield with a 6% gross yield estimate.

What does that mean and why should I care?

Well with a clear target amount you want to achieve and an assumption of how much yield your portfolio will give you, you can figure out how much your portfolio needs to be worth to make it happen.

Kinda.

I say kinda, because the number will still vary a lot depending on the stocks you choose to buy and when you buy them.

Your results will also vary a bit because your portfolio might yield less or more than your assumptions due to market environments or your personal trading decisions.

But I’ll attempt to calculate my situation for you guys to see an example.

There is this one stock I’ve followed for over 10 years, since I was in High school and I got my mum to buy it for me. (you can’t trade in Hong Kong until you’re 18, don’t know if it’s different in other countries) At the moment of my writing this, their price is at $4.22 HKD per share. The shares are sold in lots of 1000s.

This stock tends to hover between the range of $3 – $4 and the company tends to give out high dividends, around the 5% – 6% mark. (Their 5 year dividend yield average is currently at 6.04%)

Now, just to make things simple so you understand the logic of it, we will assume my entire portfolio consists of this one stock and nothing else. We will also need to assume all my shares are bought at the same price. Once we make these assumptions, I can begin to use the above numbers to calculate an estimate.

At 4.22 a share and at 6% gross yield, that’s 0.253 in dividends. The company can give out dividends as often as they want, but most do it once or twice a year. Let’s assume once a year.

That would mean we would need $2,009,500 HKD to invest at 4.22 a share in order to get $508,400 HKD in dividends that same year with a 6% gross dividend yield.

How do I get this number? I take my target total passive income amount (422,400 hkd). I divide it by 20 (because dividends account for 5%) and multiple it by 12 (because there’s 12 months and dividends are given out once a year) to get the total amount I want to get in NET dividends in one year; which gives me (254,200 hkd).

I multiple that by two to get the total gross dividend amount of 6%, which gives me (508,400 hkd). I take this number and divide it by the dividend amount per share to get the amount I need invested.

Now, from looking at the above, you’ll understand the logic behind the calculations, but you’ll also see that almost every number BUT my target is subject to change and therefore this number isn’t going to be 100% correct.

The most you will be able to do with this number is to use it as a starting point. The reality is, you won’t be using $2,009,500 HKD to buy one stock at one time. You will be buyings stocks here and there and gradually building up your portfolio. But having a starting point for reference is extremely helpful in getting you in the right direction for retirement planning.

($2,009,500 HKD is surprisingly not a big number. Retirement isn’t that hard to achieve guys)

Where are we at so far?

Just to make sure you’re still with me and you’re not lost from how long this post is.

Quick summary:

- You need to have a target age for retirement

- Age 35

- You need to estimate your lifespan to calculate how many years you have to prepare for the estimate duration of retirement

- Estimated lifespan = 90

- Time to prepare for this = 9 years

- 35 years of 360 balance retirement

- 20 years of conventional retirement

- You need liquid cash to act as an emergency fund for unexpected expenses

- You calculate that by 2 years worth of expenses

- $2,533,540 HKD saved by age 35

- Your emergency fund should be regularly reviewed and tweaked accordingly

- You calculate that by 2 years worth of expenses

- You need passive income to cover your regular, planned expenses in life

- You should have more than one type of passive income

- 4 types by 35 with most being online based

- Passive income streams should be able to provide your desired lifestyle at various stages of life

- $422,400 HKD per month for Hong Kong living standards

- Your assets should be reliable storers of wealth

- Eventual goal for rental income with real estate

- You should have more than one type of passive income

- Dividends from stocks will give you a reference point on how much money you need to invest

- Most portfolios will be able to gross 6% dividend yields

- My reference point is $2 million HKD

- Most portfolios will be able to gross 6% dividend yields

- Long retirements will need to be more fluid to fit your needs in life

- Early retirement will mean your needs compared to most retirees will be different

- Don’t be too pessimistic when making assumptions or you will be making your retirement harder than necessary

Other things to keep in mind if you’re young

We’re nearly done. But I thought I needed to add this part in because up to 30% of you are younger than 35 years old.

Homeownership

We have our numbers to focus on, which is great. It means we’re not running around like headless chickens anymore. But my plan above has conveniently missed out homeownership. I had included mortgage payments into my calculations as well as talked about the desire for investment properties. But I didn’t cover homeownership.

What I mean is, the downpayment for a place.

For most people planning their retirement; you will retire with a fully owned home and no debt. These two are the basic prerequisites for retirement to occur. I have zero debt, but I also don’t have a property under my name as of current. And in today’s property market in Hong Kong, I’m not too sure if I want to buy-to-live.

I interviewed my parents, who retired young and my mum said she thinks it’s vital for someone to own a property to ensure financial security to achieve retirement. It made sense. Renting a place just isn’t wise and it’s normally the biggest expense people have. That’s a lot of money.

Most people also don’t buy a property outright and will need to finance the purchase with a mortgage. The typical mortgage tenor around the world is 20 years. In Hong Kong it goes up to 30 years. This means I may be pushing myself out of a mortgage if I don’t get one by the time I reach 35.

(I’ll be 75 with a 30 year tenor if I take a mortgage out at 35…some banks will consider that too risky)

The starting prices for a place in Hong Kong right now is $4 million HKD. The housing market is likely to increase a further 20% by the end of this year. (2018)

That’s the starting price for something small, old and or in a bad location. That’s the reality. There are studio micro flats that will be 4 million also, and they qualify for 90% mortgage lending for first-time buyers (yay me, kinda…)

I’m not sure if I want to buy a property that’s so expensive for personal use. I personally don’t see it as good value for money, great for investment, but personal use…not so much.

I don’t think buying a place to live, in my situation goes along the same life narrative as the generations previous to mine. And I’m not actually sure what the narrative is right now for millennials. So, until I figure that out, I’m not going to have the mindset of buying a place to live in Hong Kong.

Buying to invest and buying to rent out in other places around the world are options that I am sure about though. However, a lot of research needs to be done and that would be a separate post on its own.

But I did add in mortgage estimates when calculating my desired passive income amount. I figured if I ever do change my mind, I can simply take the money from the stock portfolio for a down payment and make up the 5% in the other 3 kinds of passive income.

And that’s what I want to point out to you. Your plan should be fluid and flexible to your needs. Don’t make it too rigid. Your plans should give yourself alternative options if the situation calls for it. Because we’re not psychics, we don’t know what the future is going to be like.

Marriage and kids

Normally you don’t see marriage or kids in a retirement planning article because the target demographic consist of married parents. But I’m a typical millennial, I’m not married, no mortgage and zero kids. There’s a lot of “life milestones” I have yet to reach, which means I need to include it when planning.

I’m currently in a long term relationship but our finances are far from fully merged together. Nowhere near the point where I would be planning my retirement together with her.

That’s not to mean that won’t ever happen, but for anyone who is planning for retirement and isn’t married (like me), you’ll need to plan with the assumption that you may need to fully take care of your partner financially in the future.

It’s just too risky to make any assumptions on what your future, forever after partner will be able to provide to the situation. You’ll be putting yourself at risk of being unprepared if you make these assumptions in life.

However, if you’ve found the one and you’re both on the same page when it comes to retirement goals, you should be having honest transparent conversations with your partner.

Two people planning for retirement is so much easier to achieve, than one person alone.

That means, I fully accept that I will most likely come back to this retirement plan sometime within the next 9 years to re-do the whole thing, because my circumstances will have changed.

Another change that will bring is the possibility of kids. Again, I included modest numbers into my calculations to cater the possibilities of kids and having myself be the only financial support. The numbers I included will definitely need to be revised as situations change.

But the point is, if you’re currently childless but have intentions of having kids in the future; you need to include it in to your calculations. And although that number won’t be accurate, it won’t leave you completely unprepared when the time comes.

Most importantly, it won’t completely derail your retirement plans if you DO have added expenses in your life.

Don’t forget to Pin this to Pinterest or share it to anyone who needs some direction in how to plan for retirement. You can also sign up to my newsletter up top on the right hand side for cool emails. I share exclusive discounts on passive income business tools and services, latest post summaries and just nice updates you’ll want to read.